Table of Contents

The global Kitchen Faucet Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

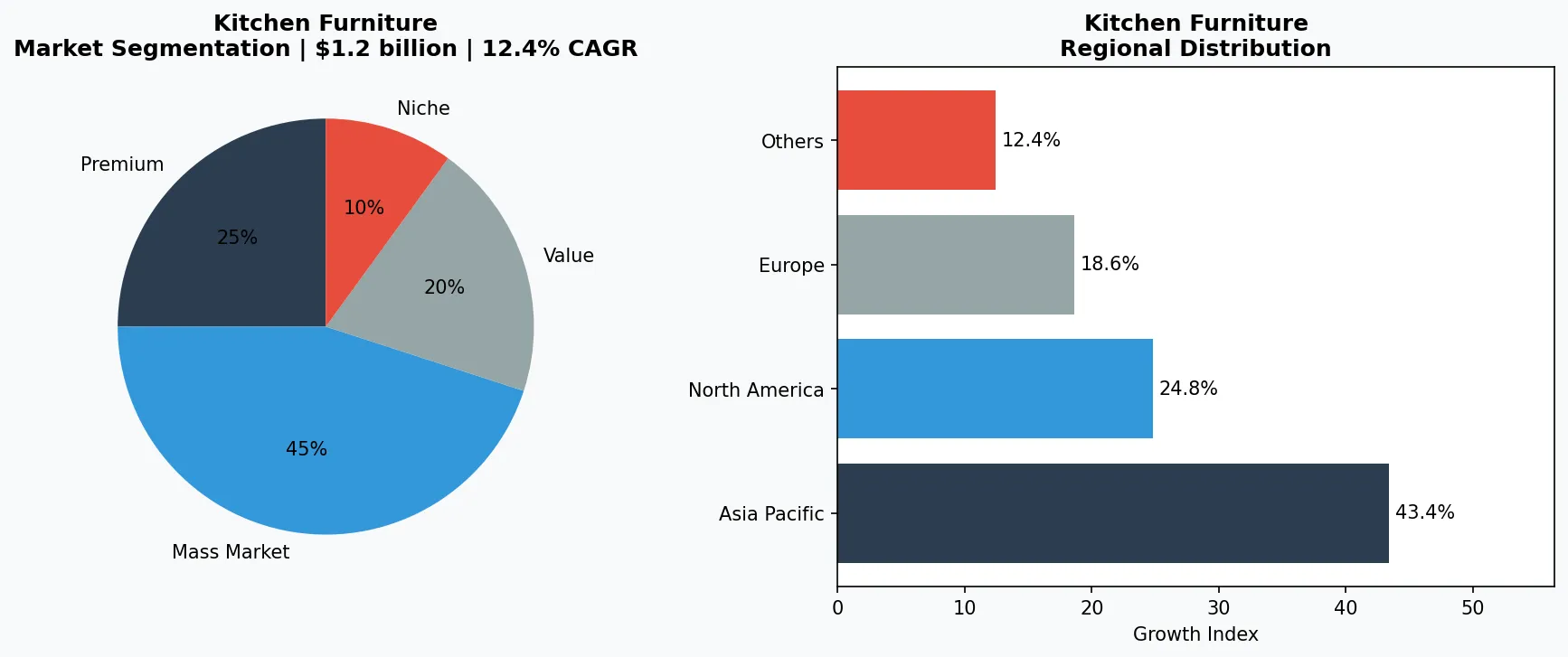

By 2026, the kitchen faucet will no longer be a passive fixture. It is becoming the command center of the modern kitchen—a hub of touchless technology, mixed-metal aesthetics, and integrated workstation functionality. The global kitchen faucet market, currently valued at approximately $1.2 billion, is projected to grow at a remarkable 12.4% CAGR through 2033, driven by a convergence of home improvement activity and shifting design priorities. Within this surge, the pull-down and pull-out faucet segment alone is capturing outsized demand: 42% of kitchen renovations now specify these flexible spout designs, according to recent trade surveys. This growth is not merely about convenience; it reflects a fundamental rethinking of how water delivery interacts with cabinetry, sinks, and daily workflow. The kitchen faucet has become a strategic product category within the broader Kitchen Furniture industry, linking storage, countertop prep zones, and clean-up areas into a seamless experience. For B2B buyers and suppliers, understanding the distinct types—from touchless smart models to traditional gooseneck designs—is essential to capturing share in a market where finish and function are increasingly inseparable.

Industry Scope & Characteristics

Integrated Design Ecosystem

Kitchen faucet types increasingly function as part of a coordinated system with workstation sinks, cabinetry hardware, and smart home controls. Pull-down models with high arcs are specifically engineered to clear sink accessories like cutting boards and drying racks.

Finish-Driven Supply Chain

Manufacturing flexibility in finishes—from aged brass to matte black—is a key differentiator. Suppliers must maintain diverse coating lines and rapid changeover capabilities to meet the mixed-metals trend without inflating lead times.

Certification Standards for Smart Faucets

Touchless and smart faucets require compliance with NSF/ANSI 61 (drinking water safety) and UL 1951 (electrical safety for plumbing products). B2B buyers should verify these certifications to avoid liability in commercial or residential installations.

Sensor and Valve R&D

Innovation is concentrated on infrared sensor accuracy and solenoid valve durability. Delta's Touch2O technology uses capacitive touch, while Moen embeds flow sensors for leak detection—both pushing the boundary of faucet intelligence beyond simple on/off control.

Key market segments and growth drivers in the Kitchen Faucet Types sector.

2. Market Analysis

The kitchen faucet market's $1.2 billion valuation in 2025 is not static; it is accelerating at a 12.4% CAGR that will push the segment past $2.5 billion by 2033. Three forces are driving this expansion. First, the rise of home improvement and renovation activity: 42% of kitchen remodels now include the specification of a pull-down or pull-out faucet, reflecting consumer preference for flexible, high-arc designs that accommodate large pots and deep sinks. This behavioral shift has made pull-down faucets the fastest-growing sub-segment within the market. Second, the integration of smart home technology is expanding the addressable market. Touchless faucets, which use motion sensors to activate water flow, are moving from premium niches to mainstream adoption, with 2026 projected as the year they cross 25% of new kitchen installations. Third, the finish and material innovation cycle is compressing replacement cycles. The emergence of aged brass as a 2026 trend, alongside matte black and brushed gold, is encouraging homeowners to upgrade even functional faucets for aesthetic reasons. For suppliers, this means that inventory strategies must now account for both functional (pull-down, touchless) and finish-driven (mixed metals, bold colors) demand vectors simultaneously.

Market segmentation and regional distribution analysis for Kitchen Faucet Types.

3. Product Categories

Kitchen faucets today fall into four dominant product types, each serving distinct operational and aesthetic needs. **Pull-Down and Pull-Out Faucets** remain the workhorses of the segment. Pull-down models feature a retractable spray head that docks into the spout, offering high reach and dual-function spray patterns—ideal for workstation sinks. Pull-out variants, with a side-mounted spray head, are preferred for smaller sinks. Together, they command roughly 42% of new installations. **Touchless and Smart Faucets** represent the fastest-growing category, leveraging infrared or capacitive sensors to enable hands-free operation. These models often include voice control integration and flow-rate monitoring, appealing to hygiene-conscious consumers and smart-home adopters. **Commercial-Style Spring Faucets** have crossed over from restaurant kitchens into residential spaces, characterized by a high-arc gooseneck and coiled hose. Their industrial aesthetic pairs well with farmhouse sinks and open shelving. **Traditional Two-Handle Faucets** persist in period-style kitchens, often specified in aged brass or oil-rubbed bronze finishes. While lower in volume growth, they maintain a loyal base among renovation projects targeting heritage or transitional design schemes.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Three key players dominate the kitchen faucet landscape, each with distinct strategies. **Kohler** leverages its integrated kitchen ecosystem, pairing touchless faucets with its workstation sink line. In 2026, Kohler is pushing mixed-metal collections—matching faucet finishes with cabinet hardware and sink accessories—to capture the coordinated-finish trend. **Moen** has bet heavily on smart technology, with its U by Moen line offering voice-controlled water delivery and leak detection. Moen's strategy targets the 42% of renovators who prioritize convenience, bundling faucets with its Flo smart water monitor. **Delta Faucet** focuses on hygienic innovation, with Touch2O technology that activates water flow via a tap on the spout body. Delta is also investing in finishes that resist fingerprints and tarnish, responding to consumer demand for low-maintenance surfaces. These players collectively control over 60% of the North American market, but regional suppliers in Europe and Asia are gaining ground by offering faster customization in finishes like aged brass and matte black.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

5. Market Trends

1. TREND_1: Touchless and Smart Faucets

Motion-sensor and voice-activated faucets are moving from luxury to mainstream. Why it matters: hands-free operation reduces cross-contamination and improves workflow in high-use kitchens. Moen's U by Moen line exemplifies this trend, integrating with Amazon Alexa and Google Assistant for precise water temperature and volume control. | TREND_2: Mixed Metals and Coordinated Finishes | 2026 kitchen design increasingly mixes faucet finishes with cabinet hardware, sink accessories, and lighting. Why it matters: this breaks the one-finish rule, allowing designers to use aged brass faucets alongside stainless steel sinks. Kohler's mixed-metal collections offer matching faucets, bar pulls, and sink grids in coordinated but contrasting tones. | TREND_3: Aged Brass Finishes | After years of dominance by brushed nickel and chrome, aged brass is the breakout finish for 2026. Why it matters: it bridges traditional and modern aesthetics, adding warmth to white and gray cabinetry. Delta Faucet has expanded its aged brass offerings across multiple faucet types, from pull-down to bridge-style models. | TREND_4: Workstation Sink Integration | Faucets are being designed specifically for workstation sinks, which feature built-in ledges for cutting boards, colanders, and drying racks. Why it matters: the faucet must clear these accessories while providing full sink access. Pull-down models with high arcs and retractable hoses are the preferred type for this application.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities define the immediate horizon. First, suppliers should prioritize touchless faucet SKUs with aged brass and matte black finishes to capture the 2026 renovation wave. The 12.4% CAGR is heavily weighted toward smart and mixed-metal categories. Second, B2B buyers should seek partnerships with manufacturers offering short-run customization in finish and spout configuration, as the demand for personalized, non-stock designs grows among high-end kitchen studios. One concrete risk: supply chain constraints for electronic components—particularly sensors and solenoid valves used in touchless faucets—could delay delivery timelines for smart models. Buyers should verify lead times and component sourcing with suppliers before committing to large orders. For the Kitchen Furniture industry, the faucet is no longer an afterthought; it is a strategic category that links storage, prep, and cleanup into a unified design statement.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Kitchen Faucet Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-10. All market figures are estimates and may vary from actual results.