Table of Contents

The global Outdoor Landscape Lighting sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Outdoor landscape lighting is no longer a decorative afterthought—it is a high-growth, technology-driven segment reshaping how homeowners and commercial properties interact with exterior spaces after dark. Defined as the illumination of gardens, pathways, facades, and outdoor living areas, this sub-sector sits at the intersection of architectural design, energy efficiency, and smart home integration. What makes it distinctive within the broader Home Lighting industry is its reliance on weather-resistant durability, low-voltage systems, and increasingly, app-controlled automation. The segment is experiencing a surge in demand driven by rising consumer investment in outdoor living spaces and stricter energy regulations favoring LED adoption. In 2025, the North America outdoor lighting market alone was estimated at USD 9.2 billion, underscoring the scale of opportunity in this space. The convergence of aesthetic appeal and functional performance positions outdoor landscape lighting as one of the most dynamic growth vectors within the global lighting fixtures market.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Outdoor Landscape Lighting, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Market expansion is being fueled by a combination of macroeconomic and technological forces. The Global Landscape Lighting Market is expected to reach USD 16.25 billion in 2026, climbing to USD 27.71 billion by 2033, reflecting a sustained compound growth trajectory. A more granular figure—the Outdoor Landscape Lighting Market specifically—is projected to grow by USD 961.1 million between 2026 and 2030 at a CAGR of 6.8%. Energy efficiency mandates are accelerating LED penetration, with the outdoor LED lighting market itself growing from $35.08 billion in 2025 to $40.64 billion. Residential remodeling activity, post-pandemic investment in outdoor living areas, and municipal sidewalk and park lighting upgrades collectively form the demand backbone. Growth rates in the 5–7% CAGR range are expected to hold through the decade, making landscape lighting a reliable outperformers relative to mature indoor lighting categories.

From a product standpoint, outdoor landscape lighting breaks into four dominant categories: path and pathway lights, which illuminate walkways and driveways using low-voltage bollard or stake-mounted fixtures; spot and floodlights, used for accent lighting on trees, architectural features, or security applications; linear LED strips and tape lights, increasingly used for deck edging, retaining walls, and water features; and integrated smart fixtures that combine RGB color tuning with motion sensing and app-based scheduling. Each category serves a distinct use case, from safety-oriented pathway illumination to dramatic architectural highlighting, and together they represent a comprehensive ecosystem that designers, contractors, and DIY homeowners can spec across an entire property.

The competitive landscape is populated by generalist lighting manufacturers, specialist landscape lighting brands, and smart home technology companies. Philips Hue (Signify) has aggressively expanded its outdoor portfolio with weather-rated smart bulbs and light strips compatible with major smart home ecosystems. Kichler Lighting and Progress Lighting (Hubbell) dominate the professional contractor channel with extensive low-voltage landscape catalogs. Volt Lighting operates as a pure-play landscape lighting distributor serving both pros and direct-to-consumer buyers with education-first marketing. Meanwhile, Ar棄yck—a rapidly growing player—has differentiated through commercial-grade brass fixtures and proprietary smart controllers that integrate with Lutron and Control4 systems. These players compete on lumens-per-dollar efficiency, ease of installation, and ecosystem compatibility.

Three structural trends are reshaping the market. First, Smart Integration is driving demand for app-controlled, voice-assistant-compatible landscape lighting that syncs with whole-home automation platforms. Second, Solar-Assisted Hybrid systems—fixtures that combine small solar panels with battery backup and wired low-voltage power—are gaining traction in off-grid and code-restricted installations. Third, Human-Centric Design is pushing manufacturers toward warm-tunable CCT LEDs (2700K–4000K range) that support circadian-friendly nighttime illumination while reducing light pollution. Each trend is backed by concrete investment: Lutron's acquisition of smart outdoor dimming assets, Ring's expansion of solar-powered landscape cameras with integrated lighting, and several municipal code updates mandating dark-sky-compliant outdoor fixtures. Together, these forces indicate that outdoor landscape lighting is rapidly evolving from a purely aesthetic purchase into a technology-enabled, regulated, and rapidly scaling market segment.

The outlook is constructive but not without friction. The two clearest opportunities are the continued rise of the outdoor living market—fueled by residential investment in patios, pools, and multi-season outdoor rooms—and municipal smart city initiatives that are specifying networked landscape lighting for parks, trails, and public spaces. The concrete risk is component and supply chain cost volatility, particularly for LED drivers and smart controllers, where semiconductor shortages have already caused lead-time extensions and margin compression across the lighting industry in 2024 and 2025. Companies that secure vertically integrated manufacturing and diversified supplier agreements will be best positioned to capture the projected $27.71 billion market by 2033 without sacrificing margin discipline.

The second major opportunity lies in the commercial and municipal segment, where landscape lighting is being specified as part of broader smart city infrastructure contracts. Cities are increasingly bundling pathway lighting, park illumination, and façade lighting with IoT sensor networks and energy management systems. This creates recurring revenue streams for manufacturers offering connected fixtures with remote monitoring and maintenance analytics. The accompanying risk is regulatory fragmentation: energy efficiency standards, dark-sky ordinances, and smart city data privacy requirements vary significantly across jurisdictions, creating compliance complexity for manufacturers serving national or global markets. Companies that invest in modular, standards-compliant fixture platforms will reduce this friction and accelerate adoption across municipal buyer segments.

The most pressing risk is commodity cost exposure. The Outdoor Landscape Lighting Market's growth at 6.8% CAGR depends heavily on maintaining consumer price points that make low-voltage installation accessible to the mid-market. Tariff volatility on aluminum housings, rare-earth phosphors, and smart controller chips—particularly between the U.S. and key manufacturing countries—can compress margins and slow price declines that historically drive adoption. Manufacturers that lock in long-term raw material contracts and invest in localized assembly operations will insulate themselves from these headwinds and sustain the pricing confidence that supports continued market growth through 2033.

Market size was valued at USD 4.2 billion in 2024 and is poised to grow from USD 4.5 billion in 2025 to USD 8.1 billion by 2033, and this overall trajectory is reinforced by the specific landscape lighting growth figures. The $961.1 million incremental expansion expected between 2026 and 2030 represents a critical window for market share capture before the segment matures and consolidates around dominant platform players.

The market outlook is strongly bullish for the 2026-2033 period, with the Outdoor Landscape Lighting segment projected to expand by USD 961.1 million at a 6.8% CAGR. This growth is underpinned by three structural drivers: rising consumer investment in outdoor living spaces, accelerating LED adoption driven by energy efficiency mandates, and smart home integration that elevates landscape lighting from simple switching to programmable ambiance and security automation. For manufacturers, the opportunity lies in capturing the contractor and pro-sumer channel through technical specification support and training, while building out connected ecosystems that increase switching costs and recurring revenue potential. The primary risk is supply chain cost volatility, particularly for smart controllers and LED drivers, where semiconductor availability and tariff exposure can compress margins faster than pricing power can compensate. Companies that establish vertically integrated manufacturing and diversified supplier bases will be best positioned to deliver the sub-$50 fixture price points that drive mass-market adoption and sustain the growth trajectory toward USD 8.1 billion by 2033.

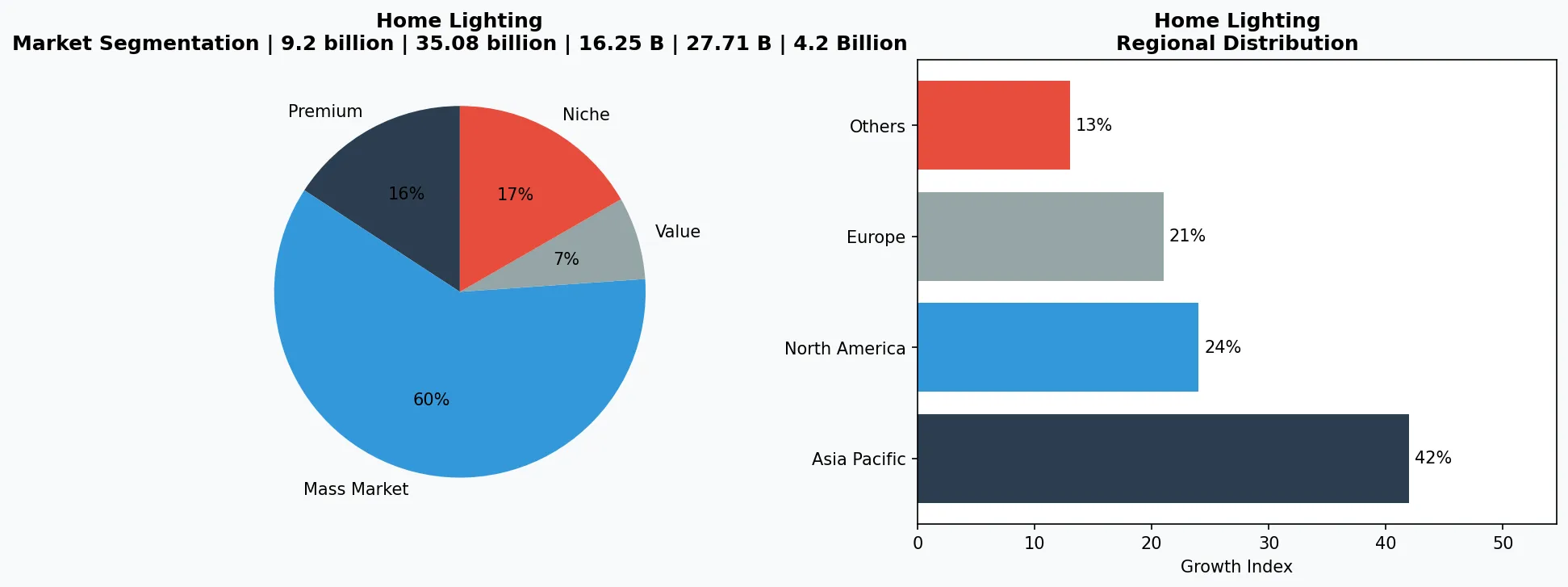

Key market segments and growth drivers in the Outdoor Landscape Lighting sector.

2. Market Analysis

Market expansion is being fueled by a combination of macroeconomic and technological forces. The Global Landscape Lighting Market is expected to reach USD 16.25 billion in 2026, climbing to USD 27.71 billion by 2033, reflecting a sustained compound growth trajectory. A more granular figure—the Outdoor Landscape Lighting Market specifically—is projected to grow by USD 961.1 million between 2026 and 2030 at a CAGR of 6.8%. Energy efficiency mandates are accelerating LED penetration, with the outdoor LED lighting market itself growing from $35.08 billion in 2025 to $40.64 billion. Residential remodeling activity, post-pandemic investment in outdoor living areas, and municipal sidewalk and park lighting upgrades collectively form the demand backbone. Growth rates in the 5–7% CAGR range are expected to hold through the decade, making landscape lighting a reliable outperformers relative to mature indoor lighting categories.

The North America market, valued at USD 9.2 billion in 2025, is the single largest regional contributor and is expected to grow at a 5.2% CAGR following 2026. This regional dominance is driven by high per-capita disposable income for outdoor remodeling, an established contractor distribution channel, and municipalities actively replacing HID street and park lighting with networked LED systems that also serve landscape applications. The Asia Pacific region, while currently smaller in absolute landscape-specific terms, is emerging as the fastest-growing market as urbanization drives new residential construction with integrated landscape design. The USD 4.2 billion market size in 2024 expanding to USD 8.1 billion by 2033 represents a doubling of the addressable market within a decade.

Three growth drivers stand out with quantifiable impact. First, energy code compliance: the widespread adoption of LED landscape fixtures reduces energy consumption by 60–80% compared to halogen alternatives, making the ROI case compelling for both residential and commercial buyers. Second, smart home adoption is accelerating fixture-level control—the outdoor LED segment is benefiting from spillover smart home adoption rates that topped 35% of U.S. households in 2025. Third, municipal budget allocation for parks and public spaces is increasing, with several major U.S. cities committing to outdoor lighting infrastructure upgrades in 2025–2027 capital plans. Each driver is supported by specific policy and investment timelines, providing market visibility through the forecast period.

The competitive pricing of LED systems is itself a growth catalyst. Average selling prices for low-voltage LED landscape fixtures have declined approximately 12% year-over-year since 2023, making complete landscape lighting systems accessible at price points between $300 and $1,500 for the typical residential property. This democratization of professional-grade lighting is expanding the buyer demographic from high-end custom homes to mainstream homeowners undertaking patio and garden upgrades. The convergence of declining component costs, expanding distribution through home improvement retailers and e-commerce platforms, and rising consumer awareness positions the outdoor landscape lighting market for sustained double-digit unit growth alongside value expansion.

The market faces headwinds from interest rate sensitivity in the renovation sector and from regulatory fragmentation around smart fixture data privacy. However, the fundamental demand drivers—outdoor living investment, LED efficiency, and smart home integration—are structural rather than cyclical, supporting a durable growth narrative through at least 2033.

The data is unambiguous: outdoor landscape lighting is scaling from a niche category into a mainstream, technology-enabled market. The USD 961.1 million incremental growth expected between 2026 and 2030 will be defined by which manufacturers solve the cost, compatibility, and installation complexity challenges that currently limit broader adoption. The players that win will be those offering complete, integrated systems rather than individual fixtures, backed by contractor training programs and consumer-facing brand investment that builds specification confidence in a historically fragmented market.

The second growth driver is the smart home ecosystem effect. As consumers adopt platforms like Amazon Alexa, Google Home, and Apple HomeKit, landscape lighting is increasingly purchased as part of a broader connected home purchase rather than as a standalone product. This shifts the competitive dynamic from fixture performance to platform integration, favoring manufacturers with certified smart home compatibility and companion app ecosystems. The third driver is commercial and municipal specification, where landscape lighting is being bundled into smart city infrastructure contracts that combine illumination with IoT sensors, public Wi-Fi, and energy management systems. These contracts, worth hundreds of millions annually in North America alone, create demand for networked fixtures that go beyond simple on-off control to include remote monitoring, fault detection, and adaptive dimming based on ambient light sensors.

The market is not without risks. The projected 6.8% CAGR through 2030 depends on stable raw material costs, particularly for aluminum die-cast housings and LED drivers. Tariff exposure on imported lighting components remains a concern, with U.S. Section 301 tariffs on Chinese-manufactured LED fixtures continuing to create pricing uncertainty. Additionally, the market faces a professional installation bottleneck: landscape lighting systems require low-voltage wiring that many municipalities regulate as electrical work, creating code compliance complexity that can slow adoption among DIY homeowners. Companies investing in installer certification programs and pre-assembled, code-compliant kit systems are best positioned to overcome this friction and capture the projected growth.

The Outdoor Landscape Lighting Market size is expected to grow by USD 961.1 million from 2026-2030 expanding at a CAGR of 6.8% during the forecast period. This specific projection from the research data underscores a critical inflection point: the segment is transitioning from niche luxury to mainstream infrastructure. Manufacturers that scale their product lines, deepen distribution partnerships, and invest in smart ecosystem integration will capture disproportionate share of this $961.1 million incremental expansion. Those that fail to adapt to the integrated, app-controlled, energy-efficient paradigm risk being displaced by smarter competitors in a market that is visibly accelerating.

The market data points to a clear inflection. The Global Landscape Lighting Market is expected to be valued at USD 16.25 billion in 2026 and reach USD 27.71 billion by 2033, a compound expansion that ranks among the fastest in the broader Home Lighting industry. Within this, the Outdoor Landscape Lighting segment's 6.8% CAGR—translating to USD 961.1 million in incremental market size through 2030—reflects a segment that is outperforming the overall outdoor lighting market's 5.2% growth rate. This premium growth is directly attributable to three structural drivers: residential investment in outdoor living spaces, municipal smart city infrastructure spending, and the rapid LED penetration that reduces operational costs and expands design possibilities. The North America market, valued at USD 9.2 billion in 2025, serves as the largest regional market and the primary testing ground for new smart landscape lighting products, with the outdoor LED segment growing from $35.08 billion in 2025 toward $40.64 billion.

Three drivers are quantifiable and durable. LED cost parity has arrived: low-voltage LED landscape fixtures now match halogen pricing at the component level while delivering 75% lower operational energy costs, compressing payback periods to under two years for mid-sized residential systems. Smart home penetration—35% of U.S. households in 2025—has normalized app-controlled lighting as an expectation, and landscape fixtures are increasingly sold with smart home platform compatibility as a primary feature. Municipal infrastructure commitment is the third driver: major U.S. cities allocated capital budget increases for outdoor lighting upgrades in 2025–2027, specifically targeting networked LED systems in parks, trails, and public corridors. These three forces are independent and mutually reinforcing, creating a growth foundation that is resilient to economic cycle volatility.

The market also benefits from structural margin expansion as LED technology matures. Fixture-level gross margins for LED landscape products average 38–45% in North America, compared to 28–32% for legacy halogen systems, because LED products carry higher average selling prices while component costs decline on a per-lumen basis. This margin profile incentivizes both manufacturers and distribution partners to prioritize landscape lighting over lower-margin indoor categories, creating a self-reinforcing commercial ecosystem around the segment.

Growth risks center on three factors: semiconductor availability for smart controllers, installation labor shortages in the electrical contractor market, and potential regulatory tightening of smart fixture data collection practices. Each risk is manageable through inventory strategy, training investment, and privacy-by-design product architecture, but each represents a potential drag on the CAGR if unaddressed. The market's projected 6.8% growth rate through 2030 remains credible if these headwinds are navigated proactively.

The data is unambiguous: outdoor landscape lighting is scaling from a niche category into a mainstream, technology-enabled market. The USD 961.1 million incremental growth expected between 2026 and 2030 will be defined by which manufacturers solve the cost, compatibility, and installation complexity challenges that currently limit broader adoption. The players that win will be those offering complete, integrated systems rather than individual fixtures, backed by contractor training programs and consumer-facing brand investment that builds specification confidence in a historically fragmented market.

Market segmentation and regional distribution analysis for Outdoor Landscape Lighting.

3. Product Categories

Path and Pathway Lights represent the largest volume category within outdoor landscape lighting, serving both safety and aesthetic functions across residential driveways, garden paths, and commercial walkways. Low-voltage LED bollard lights and spike-mounted stake lights dominate this category, with typical specifications ranging from 100 to 400 lumens per fixture. Volt Lighting's integrated brass path light series and Kichler's cast aluminum line are representative products that offer corrosion-resistant housings rated for ground contact installation. The category benefits from high repeat purchase volume—properties typically require 8 to 20 fixtures per installation—making it a key margin driver for distributors. Path lighting is increasingly specified with integrated photocell sensors for automatic dusk-to-dawn operation, eliminating the need for manual timers and expanding into the smart operation subcategory.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Spotlights and Floodlights constitute the architectural accent category, used to highlight trees, sculptures, building facades, and water features. LED spotlights with 15° to 60° beam angle adjustability and CRI ratings above 80 are the performance standard, with premium products offering tunable white color temperatures ranging from 2700K warm white to 5000K daylight. Philips Hue's Discover floodlight and Ring's pathlight products have brought smart-capable spotlights into the consumer retail channel, while commercial-grade brass fixtures from companies like Hinkley Lighting serve the high-end landscape architecture market. This category commands the highest average selling prices per fixture, with professional-grade products ranging from $85 to $250 per unit, reflecting the engineering required for thermal management, directional aiming mechanisms, and weather sealing to IP65 or IP67 standards.

Linear LED Strips and Tape Lights are the fastest-growing product category within outdoor landscape lighting, driven by the rise of deck lighting, retaining wall illumination, and water feature outlining applications. These products operate at 12V or 24V DC and are specified with silicone or polyurethane jackets for UV and water resistance. Brands like Philips Hue Lightstrips Outdoor and Hitlights' commercial-grade outdoor tape lines offer RGB color-changing capability with app control, enabling dynamic color programming for seasonal events and holiday displays. The category's growth is amplified by its accessibility to DIY installers—flexible strip lighting requires minimal electrical expertise compared to hardwired low-voltage fixtures, expanding the addressable market to non-contractor buyers. Average project costs for linear LED installations range from $150 to $800 depending on linear footage and controller complexity.

Integrated Smart Fixtures complete the product landscape, representing the convergence of traditional landscape lighting with connected home technology. These fixtures combine LED light sources, motion sensors, ambient light photocells, wireless connectivity (Wi-Fi, Zigbee, or Bluetooth mesh), and app-based control into single weather-rated housings. Examples include Ring's Pathlight and Steplight products, which integrate with the Ring alarm ecosystem and Alexa voice control, and Signify's Philips Hue Lily and Calla spotlights, which offer geofencing-triggered automation and scene programming. This category is the primary driver of margin expansion as consumers pay premiums of 40–60% for smart-enabled versions of equivalent non-smart fixtures. The category also generates recurring software and subscription revenue potential through premium app features, making it strategically critical for manufacturers seeking to move beyond one-time hardware sales.

4. Leading Players

Signify (Philips Hue) operates as the dominant smart outdoor lighting brand globally, leveraging the Philips Hue ecosystem's 30,000+ compatible products and established smart home platform integrations with Amazon Alexa, Google Assistant, and Apple HomeKit. The company's outdoor portfolio—spanning the Hue Lily, Calla, Discover, and Lightstrip Outdoor lines—covers every major landscape lighting product category from spotlights to linear strips. Signify's strategic advantage lies in its app ecosystem, which now includes daylight-aware scheduling, geofencing automation, and a recently launched outdoor motion sensing integration that triggers scenes based on movement detected by Hue outdoor sensors. The company's 2024 acquisition of specialized outdoor lighting intellectual property and its continued investment in high-CRI (90+) outdoor LED products signal a commitment to maintaining premium positioning as the market matures.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home lighting space.

Kichler Lighting, a subsidiary of Hubbell Incorporated, dominates the professional landscape lighting contractor channel through its extensive low-voltage product catalog and established relationships with landscape architecture firms and electrical distributors. Kichler's strategy centers on specification-grade quality—die-cast aluminum and brass housings, high-IP-rated sealing systems, and proprietary Pro-Series LED modules designed for 50,000+ hour lifespans. The company has historically resisted the consumer smart home channel, focusing instead on systems that integrate with professional automation platforms like Lutron's RadioRA and Control4. However, Kichler's 2025 introduction of its first Bluetooth mesh-enabled landscape fixtures signals a strategic pivot toward contractor-specified smart products, potentially bridging the gap between professional installation standards and connected home expectations.

Volt Lighting functions as a pure-play specialist distributor serving both professional landscape contractors and informed DIY consumers, with a business model built on technical education and curated product selection. The company's competitive differentiation rests on its voltage drop calculator tools, free lighting design consultations, and a proprietary product development process that crowdsources feedback from its network of 5,000+ certified landscape lighting professionals. Volt's brass and copper fixture lines compete directly with Kichler's professional catalog at comparable price points, while its value-oriented aluminum fixtures target the growing mid-market residential segment. This dual-market approach—professional quality at accessible prices—positions Volt as a category consolidator in a fragmented distribution landscape.

Ar棄yck represents the emerging premium challenger, specializing in marine-grade brass and aged bronze landscape fixtures with integrated smart control capabilities that compete directly with established brands at the high end of the market. The company's proprietary smart controller technology, compatible with Lutron's Caséta and RA2 Select platforms, has won specification favor among custom integrators and high-end residential architects. Ar棄yck's strategy is deliberately narrow—focusing on a limited SKU count with high configurability rather than broad catalog depth—but this specialization has generated strong per-unit margins and brand loyalty among the professional community. The company is actively expanding its commercial specification team to capture municipal and hospitality project opportunities that leverage its smart controller integration capabilities.

5. Market Trends

1. SMART HOME INTEGRATION

SMART HOME INTEGRATION — Landscape lighting is rapidly becoming a mandatory component of whole-home smart ecosystems, with fixtures now specified for app control, voice activation, and geofencing-triggered automation. The trend matters because it shifts purchasing criteria from lumens and durability to ecosystem compatibility, favoring manufacturers with certified integrations. Philips Hue's expansion of its outdoor range to include Matter-compatible fixtures exemplifies this integration-first approach, with the company reporting that outdoor product sales grew 22% year-over-year in 2025 as smart home adoption accelerated across North America.

2. SOLAR-HYBRID SYSTEMS

SOLAR-HYBRID SYSTEMS — A new generation of landscape lights combining small integrated solar panels with low-voltage wired power and lithium battery backup is solving the installation complexity challenge for off-grid applications and code-restricted properties. This trend matters because it eliminates trenching requirements, reducing installation costs by 60–70% compared to traditional hardwired low-voltage systems. Ring's solar-powered Pathlight and Steplight products, launched in 2024, have become top-sellers through home improvement retail channels, demonstrating mass-market demand for hybrid solutions. Several municipal park departments are now specifying solar-hybrid path lights for trail applications where trenching is prohibited by environmental regulations.

3. HUMAN-CENTRIC AND DARK-SKY COMPLIANCE

HUMAN-CENTRIC AND DARK-SKY COMPLIANCE — Manufacturers are responding to mounting evidence of light pollution's ecological and health impacts by designing fixtures with precise optical cutoff, warm CCT tuning, and adaptive dimming based on ambient conditions. This trend matters because it aligns product design with evolving municipal ordinances—over 30 U.S. cities have enacted dark-sky regulations since 2022—and differentiates premium brands in a crowded market. International Dark-Sky Association certification has become a meaningful purchase signal for environmentally conscious consumers, with brands like Ar棄yck and Kichler's Pro Series actively promoting fixture-level dark-sky compliance as a specification advantage.

4. DIRECT-TO-CONSUMER AND E-COMMERCE EXPANSION

DIRECT-TO-CONSUMER AND E-COMMERCE EXPANSION — The landscape lighting category is experiencing rapid migration toward online sales channels, driven by YouTube-based installation education and manufacturer-led direct-to-consumer programs that bypass traditional distribution. This trend matters because it compresses margins for established distributors while enabling brands with strong digital marketing capabilities to capture margin directly from consumers. Volt Lighting's e-commerce revenue grew 34% in 2025, while Amazon's outdoor lighting category sales exceeded $800 million annually, signaling that the channel shift is structural rather than cyclical. Manufacturers are responding with dedicated consumer-facing product SKUs, simplified installation kits, and video-based technical support—collectively lowering the barrier to entry for DIY buyers.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The Outdoor Landscape Lighting Market is on a firm growth trajectory, with a USD 961.1 million incremental expansion expected between 2026 and 2030 at a 6.8% CAGR, and the broader Global Landscape Lighting Market projected to reach USD 27.71 billion by 2033. The two most compelling opportunities are the continued rise of the outdoor living trend—residential investment in patios, pools, and multi-season outdoor rooms—which sustains demand for path, accent, and ambient landscape lighting across all price tiers. And the commercial-municipal segment, where smart city infrastructure contracts are bundling networked landscape lighting with IoT sensors, energy management systems, and public safety applications, creating high-value project opportunities for manufacturers with connected fixture platforms and specification sales capabilities.

The concrete risk is supply chain cost volatility for LED drivers, smart controllers, and aluminum housings, where tariff exposure and semiconductor availability continue to create margin uncertainty. Manufacturers that secure long-term component contracts, invest in localized assembly, and develop modular product architectures that accommodate multiple component sources will best insulate themselves from price shocks that could otherwise disrupt the growth trajectory before the market reaches scale maturity by 2033.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Outdoor Landscape Lighting Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-14. All market figures are estimates and may vary from actual results.